What is "Investor Protection" under the "Investor Protection Fund System?"

In case a bank, insurance company, or securities firm fails, a system (safety net) to protect customers' assets and contracts is in place, based on the laws from the viewpoint of "depositor protection," "policyholder protection," and "investor protection," respectively.

As the safety net for securities firms to protect investors, dual systems are in place to ensure that the cash and securities deposited by customers (investors) with securities firms are returned to customers: (1) a separate management system and (2) an investor protection fund system in case customers' assets cannot be returned.

The "investor protection" referred to here is intended to return the assets entrusted by customers to those customers. Even in the event of a securities firm failure, the customer assets can be returned as long as they are properly separated and managed. If the separate management of assets is not properly observed, the investor protection fund will provide compensation up to a defined limit.

Compensation by the investor protection fund will only be made in the event that the return of the customer assets is not successful.

Investor protection mechanism (1)

Securities firms must strictly observe the separate management system that is required by law.

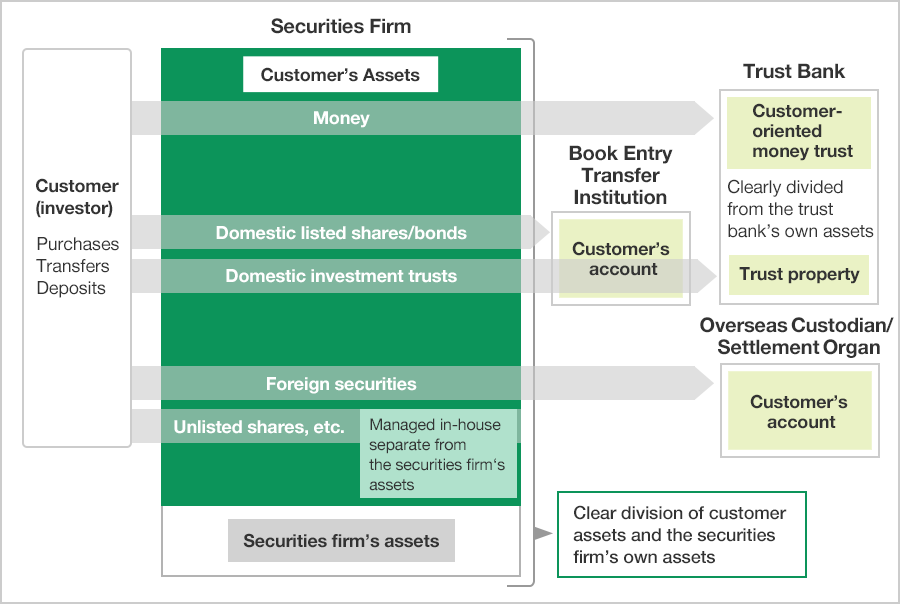

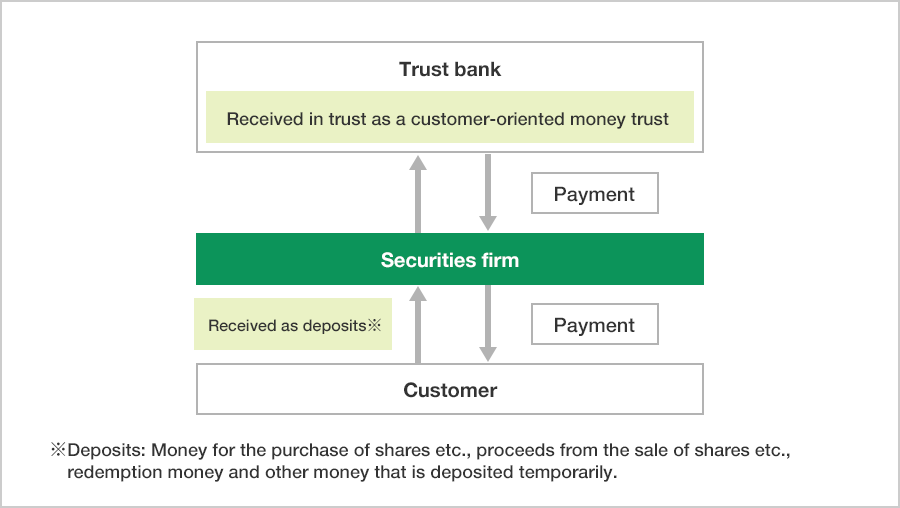

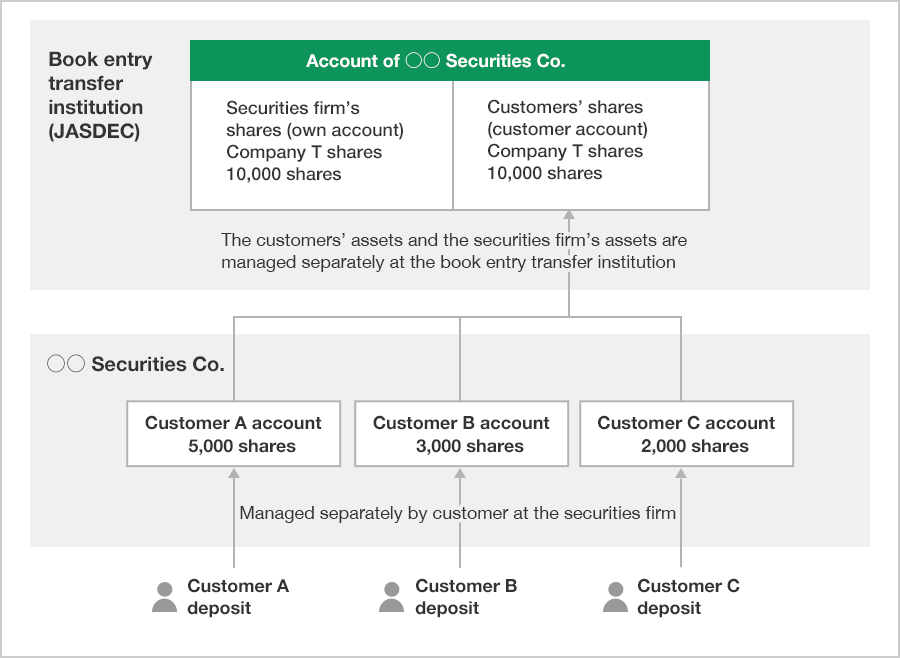

Separate management is a system whereby securities firms manage the assets entrusted by customers (cash, shares, bonds, and other securities) strictly separately from their own property to preserve the customer assets.

As long as separate management is observed, even if a securities firm goes bankrupt, this will in principle have no effect on customer assets and customers can request return of their assets from the bankrupt securities firm.

Customer (investor) assets are protected by separate management

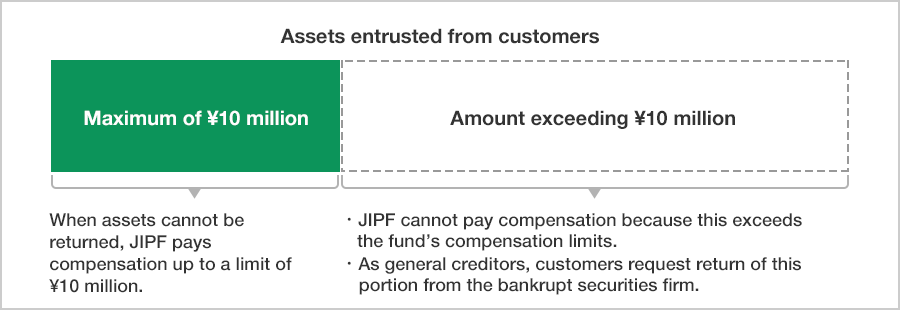

Even in the worst case, customers can receive up to ¥10 million in compensation.

In the unlikely event that a securities firm goes bankrupt, if the securities firm appropriately complies with the requirement of separate management of customers’ assets, all assets deposited with the securities firm by customers can basically be returned to the customers.

However, if the securities firm does not comply with the separate management system and cannot smoothly return customer assets, the Japan Investor Protection Fund (hereinafter referred to as “JIPF”) will pay the customer the amount of assets that cannot be returned, converted at the market value on the day JIPF publicly announces that it will provide compensation (up to 10 million yen per customer).

Please note that JIPF will not provide compensation if customers’ cash or securities are properly segregated and managed by a securities firm.

For example, even if the price of securities declines, JIPF will not provide compensation if the securities firm manages customers’ assets are properly segregated (JIPF does not cover the loss caused by the decline in price).

If the securities become worthless due to the bankruptcy of the issuer of the securities, or if the issuer defaults on its obligations and fails to pay principal or interest, JIPF will not provide compensation if the securities are properly segregated (a customer’s rights will be handled in the bankruptcy proceedings of the issuer).

JIPF will not cover losses incurred due to the securities firm's failure to provide appropriate explanations when selling securities, if the securities firm manages the securities in a segregated manner (JIPF is not an institution to cover losses due to fraudulent acts in general).

Some securities firms may handle financial instruments that are not covered by JIPF (e.g., over-the-counter derivatives transactions, crypto assets, etc.). For more information, please refer to Q&A.

JIPF Compensation Limits

Customer assets are protected by dual systems.

In this way, assets which customers entrust to securities firms are protected by the dual systems of separate management by securities firms and compensation by JIPF.

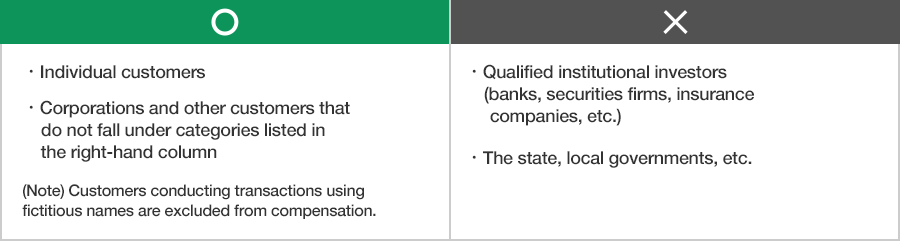

Investors we protect

JIPF protects general customers, excluding professional investors.

JIPF protects customer transactions, within a certain range.

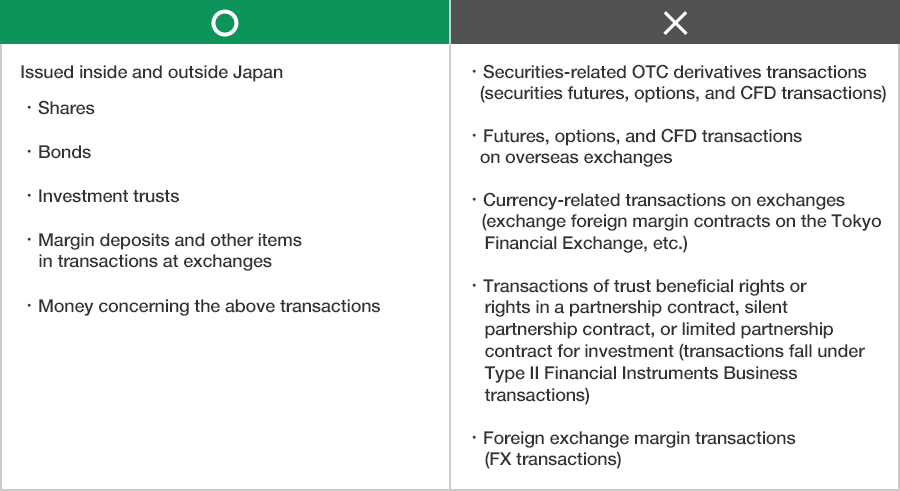

Transactions we protect

JIPF protects assets (money and securities) entrusted by general customers to securities firms in transactions concerning the securities-related business or the market commodity derivatives-related business.

Transactions we cannot protect

JIPF cannot protect over-the-counter derivatives transactions and foreign market derivatives transactions, even those concerning the above-stated businesses.

JIPF cannot protect transactions that fall under the Type II Financial Instruments Business, such as those concerning trust beneficial rights, partnership agreements, anonymous partnership agreements, or limited partnership agreements.

JIPF cannot protect against a decline in the value of customer securities.